Matt Lentzner, Janine Jagger and I have designed a survey for participants of Gluten-free January, using the online application StatCrunch. Janine is an epidemiologist who studies healthcare worker safety at the University of Virginia; she has experience designing surveys for data collection so we're glad to have her on board. The survey will allow us to systematically gather and analyze data on the results of Gluten-free January. It will be 100 percent anonymous-- none of your answers will be connected to your identity in any way.

This survey has the potential to be really informative, but it will only work if you respond! The more people who take the survey, the more informative it will be, even if you didn't avoid gluten for a single day. If not very many people respond, it will be highly susceptible to "selection bias", where perhaps the only people who responded are people who improved the most, skewing the results.

Matt will be sending the survey out to everyone on his mailing list. Please complete it, even if you didn't end up avoiding gluten at all! There's no shame in it. The survey has responses built in for people who didn't avoid gluten. Your survey will still be useful!

We have potential data from over 500 people. After we crunch the numbers, I'll share them on the blog.

Monday, January 31, 2011

Cat Comes To Town

The best part about our photo shoot was that she was game to do about anything. When I was in Cape Cod a few years ago, I took a bunch of timed jumpie pics as the sun was setting. If you need an activity to look crazy in front of people and laugh at yourself, this is a good one to try. It is stupid and is great for a good laugh and some fun photographs. Also, Cat is not as fond as birds as I am. She was even willing to walk around a flock of birds and run towards them to try and get a shot of them surrounding her. The one where she is standing still is a moment of her thinking, "Really? You want me to do what with the birds?" to the shot where she casually jogged through them, not missing a beat. Some of the best times you can have with a friend is being silly with a camera.

I haven't made the time to take my camera out to take photographs lately so it was a nice change of pace to do that again while we toured around. Here are some photographs from our time last week.

Sunday, January 30, 2011

Bernanke, Benanke, Bernake, Burnake, Burn

I find it rather interesting that I have found so many different ways of misspelling his name. In a funny way I think that is representative of the absolutely high esteem in which I hold him. For all my Bernanke misspellings I apologize to you. If Ben or his buddies happen read this - the misspellings were intentional...Better to have a spelling problem in a math business than a logic problem in the Banking business.

Saturday, January 29, 2011

Coming soon to a country near you...

Bernanke has blood on his hands...

In November I posted this post and this chart. Bubblicious "Bernanke Span Krudman" Baby... I indicated that if indeed Bernanke had the gall to pursue a policy of price and market manipulation in commodity and inflationary assets that the potential outcome would likely be of the worst possible in nature rather than something hopefully less extreme.

To tell you the truth, I did not think that it would even have been possible for a sane person to impart that initiative onto the markets in the manner and to the extreme that Mr Bernanke has. Bernanke has single handedly destroyed trust and faith in the markets, compromised trust and faith in fundamental life for the public and spread his virus to the whole global system for the sake of a few banking buddies.

Bernanke is responsible for the riots and social revolution in the middle east. Granted there is a lot of pent up emotion over there, but what pent up emotions need are sparks. Bernanke provided much more than Sparks by trying to pump balance sheets of banks at the expense of people. But we can see that what happens here does not just stay here. The perception of there being a reason to hoard and accumulate inflationary assets has been much stronger and misplaced than I thought it ever could be. That action and perception has been directly influenced by Bernanke and Co. That activity has distorted the perception of supply, demand and price dynamics.

Bernanke and the Fed's only business is manipulating numbers. That is all they do. Which is why they have directly manipulated economic indexes that are used in calculating GDP...GDP came in at 3.2%. The target was 3.5% - so we missed. The fact that the number are magically seasonally, secondarily and arbitrarily adjusted means that we can not rely on the official numbers. Additionally, if we were to calculate inflation correctly as well as other metrics and the number would have come in closer to 1.2%. This game is a farce. Now if that was it - that would be enough...however we had a horrible GDP number, significant earnings report issues yet...the markets defy them as they continue to celebrate the Bernake put. Bernanke knows that a market that goes up on bad news is perceived as much more bullish than any other...so the powers that be jump on that to squeeze shorts and embolden leveraged buyers. "If the market can't go down on that news, then this time its different - trade on maximum leverage." or so goes the average investor. However, trust in the market is not created by this kind of aberration and yesterday TRUST was breached and ironically had NOTHING to do with Egypt in my opinon. What I saw as I was shorting the market this am was total confusion. Shorts were totally confused. "Why are we making new highs? Who is buy this crap?" Longs were confused: "Why are we making new highs? Why am I on 10x margin? Who is buying? Where is Bernanke? The answer came swiftly. I expect that the margin level will finally begin to decline from the highest in years at $276.6 billion. But, Bernanke has succeeded in lulling people into a ridiculous complacency...he has increased the risk for EVERY sector of the financial system. And now the results of this trust and risk issues are spreading throughout the world...he has blood on his hands in addition to mush for brains.

Watch the video below. When central planners insist on stealing from the public this is the result and it will be coming soon to a location much closer to me and you that we may have every thought possible.

Thursday, January 27, 2011

The Diabetes Epidemic

The CDC just released its latest estimate of diabetes prevalence in the US (1):

These data are self-reported, and do not correct for differences in diagnosis methods, so they should be viewed with caution-- but they still serve to illustrate the trend. There was an increase in diabetes incidence that began in the early 1990s. More than 90 percent of cases are type 2 diabetics. Disturbingly, the trend does not show any signs of slowing.

The diabetes epidemic has followed on the heels of the obesity epidemic with 10-20 years of lag time. Excess body fat is the number one risk factor for diabetes*. As far as I can tell, type 2 diabetes is caused by insulin resistance, which is probably due to energy intake exceeding energy needs (overnutrition), causing a state of cellular insulin resistance as a defense mechanism to protect against the damaging effects of too much glucose and fatty acids (3). In addition, type 2 diabetes requires a predisposition that prevents the pancreatic beta cells from keeping up with the greatly increased insulin needs of an insulin resistant person**. Both factors are required, and not all insulin resistant people will develop diabetes as some people's beta cells are able to compensate by hypersecreting insulin.

Why does energy intake exceed energy needs in modern America and in most affluent countries? Why has the typical person's calorie intake increased by 250 calories per day since 1970 (4)? I believe it's because the fat mass "setpoint" has been increased, typically but not always by industrial food. I've been developing some new thoughts on this lately, and potentially new solutions, which I'll reveal when they're ready.

* In other words, it's the best predictor of future diabetes risk.

** Most of the common gene variants (of known function) linked with type 2 diabetes are thought to impact beta cell function (5).

Diabetes affects 8.3 percent of Americans of all ages, and 11.3 percent of adults aged 20 and older, according to the National Diabetes Fact Sheet for 2011. About 27 percent of those with diabetes—7 million Americans—do not know they have the disease. Prediabetes affects 35 percent of adults aged 20 and older.Wow-- this is a massive problem. The prevalence of diabetes has been increasing over time, due to more people developing the disorder, improvements in diabetes care leading to longer survival time, and changes in the way diabetes is diagnosed. Here's a graph I put together based on CDC data, showing the trend of diabetes prevalence (percent) from 1980 to 2008 in different age categories (2):

These data are self-reported, and do not correct for differences in diagnosis methods, so they should be viewed with caution-- but they still serve to illustrate the trend. There was an increase in diabetes incidence that began in the early 1990s. More than 90 percent of cases are type 2 diabetics. Disturbingly, the trend does not show any signs of slowing.

The diabetes epidemic has followed on the heels of the obesity epidemic with 10-20 years of lag time. Excess body fat is the number one risk factor for diabetes*. As far as I can tell, type 2 diabetes is caused by insulin resistance, which is probably due to energy intake exceeding energy needs (overnutrition), causing a state of cellular insulin resistance as a defense mechanism to protect against the damaging effects of too much glucose and fatty acids (3). In addition, type 2 diabetes requires a predisposition that prevents the pancreatic beta cells from keeping up with the greatly increased insulin needs of an insulin resistant person**. Both factors are required, and not all insulin resistant people will develop diabetes as some people's beta cells are able to compensate by hypersecreting insulin.

Why does energy intake exceed energy needs in modern America and in most affluent countries? Why has the typical person's calorie intake increased by 250 calories per day since 1970 (4)? I believe it's because the fat mass "setpoint" has been increased, typically but not always by industrial food. I've been developing some new thoughts on this lately, and potentially new solutions, which I'll reveal when they're ready.

* In other words, it's the best predictor of future diabetes risk.

** Most of the common gene variants (of known function) linked with type 2 diabetes are thought to impact beta cell function (5).

Two Wheat Challenge Ideas from Commenters

Some people have remarked that the blinded challenge method I posted is cumbersome.

Reader "Me" suggested:

Reader "Me" suggested:

You can buy wheat gluten in a grocery store. Why not simply have your friend add some wheat gluten to your normal protein shake.Reader David suggested:

They sell empty gelatin capsules with carob content to opacify them. Why not fill a few capsules with whole wheat flour, and then a whole bunch with rice starch or other placebo. For two weeks take a set of, say, three capsules every day, with the set of wheat capsules in line to be taken on a random day selected by your friend. This would further reduce the chances that you would see through the blind, and it prevent the risk of not being able to choke the "smoothie" down. It would also keep it to wheat and nothing but wheat (except for the placebo starch).The reason I chose the method in the last post is that it directly tests wheat in a form that a person would be likely to eat: bread. The limitation of the gluten shake method is that it would miss a sensitivity to components in wheat other than gluten. The limitation of the pill method is that raw flour is difficult to digest, so it would be difficult to extrapolate a sensitivity to cooked flour foods. You might be able to get around that by filling the pills with powdered bread crumbs. Those are two alternative ideas to consider if the one I posted seems too involved.

Wednesday, January 26, 2011

ES Swing Still Short

ES Swing may add another entry if the market were to be able to get another push...that would be a huge size entry in terms of the number of contracts. You can see the trade reticulation entries and exits on this chart it currently has 55 contracts open.

Machinations

Nothing like a bad housing report to get the markets motivated.

As addition collateral, the EURO (which I am reasonably short) has hit major resistance around the 1.3730 area. All in all the currencies, transports and some index action portray a very dangerous situation. Moreover, the rubberband has been stretched by another factor - the overshoot of our inverse head and shoulders pattern targets on the daily charts. These targets were in the range of 1240 to 1255ish for the SP500. We have overshot by more than 50 points. This creates the prospect of an overshoot in the reverse direction when a correction occurs of roughly the same amount. So, we may be in for another flash crash type thing that everyone can blame on some fat fingered button pusher who types 1 billion instead of 1 million into a special and proprietary order entry system (especially designed for reporting by CNBS media spokes people) that has no security and/or validation that would validate and verify that kind of data.

As addition collateral, the EURO (which I am reasonably short) has hit major resistance around the 1.3730 area. All in all the currencies, transports and some index action portray a very dangerous situation. Moreover, the rubberband has been stretched by another factor - the overshoot of our inverse head and shoulders pattern targets on the daily charts. These targets were in the range of 1240 to 1255ish for the SP500. We have overshot by more than 50 points. This creates the prospect of an overshoot in the reverse direction when a correction occurs of roughly the same amount. So, we may be in for another flash crash type thing that everyone can blame on some fat fingered button pusher who types 1 billion instead of 1 million into a special and proprietary order entry system (especially designed for reporting by CNBS media spokes people) that has no security and/or validation that would validate and verify that kind of data.

“Though new home sales rose by more than forecasts in December, the increase was off a very low reading in November and was primarily due to a jump in sales in one region. To put the increase in the West into perspective, unadjusted nonannualized new home sales in the West rose to 7,000 from 4,000—once annualized and seasonally adjusted, these sales are reported to have risen to 110,000 in December from 64,000 in November. While it is encouraging that sales continue to move into better alignment with home supply, we characterize new home sales as still bouncing around at low levels (December’s reading compares to a peak of 1.4 million in July 2005) and we do not expect the housing sector to be either a significant driver nor a drag on economic growth in 2011.”

Tuesday, January 25, 2011

Dollar Update - Perfect Bounce

Nice bounce around the areas that we should see it - hopefully we can breakout over the falling wedge at some point soon...FYI covering Silver and Gold here for a bounce. Up nearly $100 for Gold and $4 for silver.

Monday, January 24, 2011

Blinded Wheat Challenge

Self-experimentation can be an effective way to improve one's health*. One of the problems with diet self-experimentation is that it's difficult to know which changes are the direct result of eating a food, and which are the result of preconceived ideas about a food. For example, are you more likely to notice the fact that you're grumpy after drinking milk if you think milk makes people grumpy? Maybe you're grumpy every other day regardless of diet? Placebo effects and conscious/unconscious bias can lead us to erroneous conclusions.

The beauty of the scientific method is that it offers us effective tools to minimize this kind of bias. This is probably its main advantage over more subjective forms of inquiry**. One of the most effective tools in the scientific method's toolbox is a control. This is a measurement that's used to establish a baseline for comparison with the intervention, which is what you're interested in. Without a control measurement, the intervention measurement is typically meaningless. For example, if we give 100 people pills that cure belly button lint, we have to give a different group placebo (sugar) pills. Only the comparison between drug and placebo groups can tell us if the drug worked, because maybe the changing seasons, regular doctor's visits, or having your belly button examined once a week affects the likelihood of lint.

Another tool is called blinding. This is where the patient, and often the doctor and investigators, don't know which pills are placebo and which are drug. This minimizes bias on the part of the patient, and sometimes the doctor and investigators. If the patient knew he were receiving drug rather than placebo, that could influence the outcome. Likewise, investigators who aren't blinded while they're collecting data can unconsciously (or consciously) influence it.

Back to diet. I want to know if I react to wheat. I've been gluten-free for about a month. But if I eat a slice of bread, how can I be sure I'm not experiencing symptoms because I think I should? How about blinding and a non-gluten control?

Procedure for a Blinded Wheat Challenge

1. Find a friend who can help you.

2. Buy a loaf of wheat bread and a loaf of gluten-free bread.

3. Have your friend choose one of the loaves without telling you which he/she chose.

4. Have your friend take 1-3 slices, blend them with water in a blender until smooth. This is to eliminate differences in consistency that could allow you to determine what you're eating. Don't watch your friend do this-- you might recognize the loaf.

5. Pinch your nose and drink the "bread smoothie" (yum!). This is so that you can't identify the bread by taste. Rinse your mouth with water before releasing your nose. Record how you feel in the next few hours and days.

6. Wait a week. This is called a "washout period". Repeat the experiment with the second loaf, attempting to keep everything else about the experiment as similar as possible.

7. Compare how you felt each time. Have your friend "unblind" you by telling you which bread you ate on each day. If you experienced symptoms during the wheat challenge but not the control challenge, you may be sensitive to wheat.

If you want to take this to the next level of scientific rigor, repeat the procedure several times to see if the result is consistent. The larger the effect, the fewer times you need to repeat it to be confident in the result.

* Although it can also be disastrous. People who get into the most trouble are "extreme thinkers" who have a tendency to take an idea too far, e.g., avoid all animal foods, avoid all carbohydrate, avoid all fat, run two marathons a week, etc.

** More subjective forms of inquiry have their own advantages.

The beauty of the scientific method is that it offers us effective tools to minimize this kind of bias. This is probably its main advantage over more subjective forms of inquiry**. One of the most effective tools in the scientific method's toolbox is a control. This is a measurement that's used to establish a baseline for comparison with the intervention, which is what you're interested in. Without a control measurement, the intervention measurement is typically meaningless. For example, if we give 100 people pills that cure belly button lint, we have to give a different group placebo (sugar) pills. Only the comparison between drug and placebo groups can tell us if the drug worked, because maybe the changing seasons, regular doctor's visits, or having your belly button examined once a week affects the likelihood of lint.

Another tool is called blinding. This is where the patient, and often the doctor and investigators, don't know which pills are placebo and which are drug. This minimizes bias on the part of the patient, and sometimes the doctor and investigators. If the patient knew he were receiving drug rather than placebo, that could influence the outcome. Likewise, investigators who aren't blinded while they're collecting data can unconsciously (or consciously) influence it.

Back to diet. I want to know if I react to wheat. I've been gluten-free for about a month. But if I eat a slice of bread, how can I be sure I'm not experiencing symptoms because I think I should? How about blinding and a non-gluten control?

Procedure for a Blinded Wheat Challenge

1. Find a friend who can help you.

2. Buy a loaf of wheat bread and a loaf of gluten-free bread.

3. Have your friend choose one of the loaves without telling you which he/she chose.

4. Have your friend take 1-3 slices, blend them with water in a blender until smooth. This is to eliminate differences in consistency that could allow you to determine what you're eating. Don't watch your friend do this-- you might recognize the loaf.

5. Pinch your nose and drink the "bread smoothie" (yum!). This is so that you can't identify the bread by taste. Rinse your mouth with water before releasing your nose. Record how you feel in the next few hours and days.

6. Wait a week. This is called a "washout period". Repeat the experiment with the second loaf, attempting to keep everything else about the experiment as similar as possible.

7. Compare how you felt each time. Have your friend "unblind" you by telling you which bread you ate on each day. If you experienced symptoms during the wheat challenge but not the control challenge, you may be sensitive to wheat.

If you want to take this to the next level of scientific rigor, repeat the procedure several times to see if the result is consistent. The larger the effect, the fewer times you need to repeat it to be confident in the result.

* Although it can also be disastrous. People who get into the most trouble are "extreme thinkers" who have a tendency to take an idea too far, e.g., avoid all animal foods, avoid all carbohydrate, avoid all fat, run two marathons a week, etc.

** More subjective forms of inquiry have their own advantages.

Sunday, January 23, 2011

A Visit With John, Ellyn and Milan in Mexico

They live on a house right on the water about 35 minutes from the border. They don't have electricity, but do have propane and water. They refer to their housing community as the "camp" and everyone knows each other very well. John and Ellyn are entertainers with a traveling show so you might have seen them at your local fair or at the San Diego zoo where Ellen is "Dr. Zoolittle."

I didn't bring Max along for the ride, but I brought my cousin, Wendy. I love it when I throw out a crazy idea and people say yes. I told Wendy that I wanted to go to Mexico to meet an online friend that I've never met and she said "ok" without question.

What I like most about them is that they are energetic about everything. You can talk about all subjects and they will have a story and will give their opinion without hesitation. I felt right at home with them and love the life they both lead. They follow their passion and do what they love.

I told a few people about going to Mexico to meet a stranger and most people worried that I would be ok. I didn't think twice about it. Of course there are many reasons to be afraid to meet strangers or travel to another country to do so, but that's the exciting part about it. I didn't stay long on this trip, but I plan to go back again to soak up the experience of living at their "camp." Wendy and I were treated like family and Ellyn cooked the best meals!

It was also interesting to see that we were about the only tourists in town. I will blog about that in another post but for now, here are some photographs to give you an idea of what life is like for Ellyn, John and their dog Milan. I look forward to catching one of their performances soon.

If a company files bankruptcy...and Goldman/JPM off risk while supressing fundemental issues...

what happens? Can you say MUNI bond and Auction Rate. Well its back. Fraud on a massive scale perpetrated right in front of our eyes as if we were all too stupid to see it and most definitely not capable of stopping it and punishing the fraudsters.

In this case, a company files bankruptcy and the press conspires by avoiding to promote its formal insolvency. Obviously the press must have a reason that it would like everyone to believe that it was and has not been news worthy or relevant. Great, we can continue life as usual while everyone in the "know" does just the opposite and dumps risk. Well, wouldn't you know it, the companies that were cental to the headlines in 2007, 2008 and 2009 are insolvent and their Munibond insurance is no good - as it if ever were. While AMBAC was busy preparing its bankruptcy filing last year, Goldman Sachs was setting up its new "Ultrasafe Munibond Marketing Entity" with Incapital and JPM was trying to off risk to mom's and pops through Schwab and UBS. Lots names familiar to people who got hosed by Auction Rate securities...how come the same players are still in the same game after they blew everyone up?

Two months ago I met a guy in South Point Park in Miami Beach. He was an older guy trying to preserve money for his grand kids education - as he said. He asked me about Muni's, to which I replied that I felt "the Muni markets are rife with bad documentation, risk and fraud and at high risk for (structural) defaults. Not a great market in which to operate, especially if Goldman and JPM are pumping like mad" The funny thing was that he then asked me about this one particular munibond that I, ironically, had looked at for Hartford, Pennsylvania. Yes, you know the city that missed its bond payments and that the state had to lend 55 million to so that they could pay the interest on the notes. He was pumped this security by his broker who said it paid nearly 8% (of which he was very proud) and was fully insured. Clearly the broker gets paid a lot to sell crap and is therefore, highly incentivized to rip this guy off...He was rather shocked to find out that the reason Hartford was paying such exorbitant rates is because they are broke and can't actually make the payments. The issue of insurance seemed to bring him some comfort, as his advisor had clearly spent quite some time on that subject. But the insurance is worthless. What I saw in action was an example of the JPM and GoldmanTax's effort to further rip-off the public and transfer the wealth into their bonus packages.

When AMBAC was busy getting its bankruptcy filing prepared. Wisconsin's Office of the Commissioner of Insurance, or OCI took over AMBAC contracts and obligations without making much more than a peep...in the name of preventing a MUNI bond collapse and frozen issuance market...by doing this it was hoping to help the incompetent by deceiving the market into complacency once again while bringing no new structural stability to the picture in any way. The hope was, lets just get the AMBAC name stabilised or out of the picture and keep the game on the normally scheduled programming. Yes, the charade...was endorsed by the OCI and this is an example of regulated fraud. The fraud is all still there, its still occurring every day and these guys attempted to make sure that this was the outcome. That was their specific goal...let a totally flawed, deceptive, highly inducement oriented product continue to function with NO impediments.

Ironically, we should all already know that by its nature, a market in which someone tries to get your money by locking it up, providing crappy collateral and fuzzy or deceptive documentation, would require them to make some sort of inducements and incentives. "Ok, lets make the gains tax-free in order to find marks to whom to pawn it." Sounds logical to me.

At the very same time as this ponzi scheme is being implemented, the regulator(s) had NO problem with all the major Dealers scaling up their marketing and hype surrounding these products specifically focused on "Mom" and "Pop". Yes, there is no issue there...just lets get this boat back on the water keep it looking like its floating and get people on it...

OCI and the regulators in general did a GREAT job regulating yet another legalized fraud and theft.

In this case, a company files bankruptcy and the press conspires by avoiding to promote its formal insolvency. Obviously the press must have a reason that it would like everyone to believe that it was and has not been news worthy or relevant. Great, we can continue life as usual while everyone in the "know" does just the opposite and dumps risk. Well, wouldn't you know it, the companies that were cental to the headlines in 2007, 2008 and 2009 are insolvent and their Munibond insurance is no good - as it if ever were. While AMBAC was busy preparing its bankruptcy filing last year, Goldman Sachs was setting up its new "Ultrasafe Munibond Marketing Entity" with Incapital and JPM was trying to off risk to mom's and pops through Schwab and UBS. Lots names familiar to people who got hosed by Auction Rate securities...how come the same players are still in the same game after they blew everyone up?

Two months ago I met a guy in South Point Park in Miami Beach. He was an older guy trying to preserve money for his grand kids education - as he said. He asked me about Muni's, to which I replied that I felt "the Muni markets are rife with bad documentation, risk and fraud and at high risk for (structural) defaults. Not a great market in which to operate, especially if Goldman and JPM are pumping like mad" The funny thing was that he then asked me about this one particular munibond that I, ironically, had looked at for Hartford, Pennsylvania. Yes, you know the city that missed its bond payments and that the state had to lend 55 million to so that they could pay the interest on the notes. He was pumped this security by his broker who said it paid nearly 8% (of which he was very proud) and was fully insured. Clearly the broker gets paid a lot to sell crap and is therefore, highly incentivized to rip this guy off...He was rather shocked to find out that the reason Hartford was paying such exorbitant rates is because they are broke and can't actually make the payments. The issue of insurance seemed to bring him some comfort, as his advisor had clearly spent quite some time on that subject. But the insurance is worthless. What I saw in action was an example of the JPM and GoldmanTax's effort to further rip-off the public and transfer the wealth into their bonus packages.

SEPTEMBER 8, 2010:

Goldman Sachs Group Inc. is about to start selling municipal bonds directly to mom and pop.The New York company plans to enter a partnership this week with Chicago securities firm Incapital LLC to sell bonds issued by U.S. states, cities and towns to individual investors, according to a person familiar with the situation.

The arrangement will make billions of dollars of municipal bonds underwritten by Goldman available for sale by at least 85,000 brokers in Incapital's distribution network of broker-dealer firms.

The move allows Goldman to branch out into a lucrative area of the fixed-income markets, a haven for retail investors scared off by volatility in the stock market and riskier corporate credit markets. While some municipalities are facing budget crises, it is rare for municipal bonds to default. Such securities yield more than certificates of deposit or other ultra-safe investments and are tax-free in most cases, making them a staple in retiree savings accounts. read moreGoldman strikes deal to sell new-issue munis

October 1, 2010My question is:

Goldman Sachs Taps Retail With Munis

By Patrick McGee

The company recently announced that it is teaming up with the Chicago securities distributor Incapital LLC in an exclusive agreement to sell new-issue munis. Incapital maintains a retail distribution network of more than 600 broker-dealers and 400 fee-based advisors.

"We're really acting as Goldman's syndicate desk to the retail-dealer community during the traditional retail offer period," John Radtke, the president of Incapital, says. "It gives Goldman access to a customer base that they historically have never reached."

Goldman has been the lead underwriter on $16.3 billion of munis this calendar year, according to Thomson Reuters. It is best known in the municipal bond world for its institutional distribution, particularly for large issues-the 95 deals it has senior managed this year is the smallest number of deals among the top-10 firms.

Historically, virtually none of Goldman's underwriting has been distributed to the conventional retail base, aside from high-net-worth individuals who can purchase new municipal products through its private wealth division.

"We're helping to create something that's almost unprecedented in the municipal business," Radtke says. "And that's giving retail access to investments that they would never actually see."

Jeff Scruggs, co-head of Goldman's public-sector and infrastructure group, described the agreement as an expansion of a multiyear relationship with Incapital.

The firms have worked together for the past three years marketing Goldman's certificates of deposit, plain-vanilla corporate debt and some structured fixed-income products. The addition of municipal products deepens their ties while also offering municipal issuers the chance to market bonds to a wider investment base. "We felt that with the addition of the Incapital relationship, it really rounds out our overall marketing and distribution ability," Scruggs says.

Retail demand for tax-exempt products has been growing, as investors become more concerned with wealth preservation and protecting their portfolios from a potential increase in income tax rates. Federal Reserve data indicates that household holdings of muni debt increased to about 36% of the market in the first quarter of this year from less than 33% in the first quarter of 2008.

During that period, total outstanding muni debt grew 4.6%, to $2.83 trillion, from $2.71 trillion while household holdings surged 8.9% from $937.7 billion, to $1.020 trillion.

Earlier this summer, fixed-income analysts at JPMorgan Chase & Co. called the increase in retail demand a shift in the tectonic plates of the market that hasn't been seen since tax laws were changed in 1986.

The Goldman-Incapital agreement was six months in the making, according to Radtke, who expects it to be fully implemented this month. Incapital will distribute the new-issue bonds initially to a selected group of 175 broker-dealer firms that represent about 85,000 brokers, with assets totaling more than $4 trillion, Radtke says. However, he declined to name which firms were selected.

Incapital, founded in 2001, isn't very well known in muni land. But in the broader fixed-income world it offers underwriting and distribution for corporate debt, U.S. agency bonds, CDs, structured notes and mortgage-backed securities.

"The last item or table-leg was municipals," Radtke says of Incapital's expansion into fixed income. He notes that more than half of its broker-dealer clients are involved with municipal products.

"The muni world might not know Incapital, but munis aren't new to us, based on the personnel we have employed," Radtke says. He adds that the growing trading team alone has more than 50 years of experience.

Incapital hopes the agreement could raise its profile in the muni world, as it may begin looking to make a splash as a co-underwriter at some point in the future, Radtke says. This distribution deal doesn't preclude that, he says.

JPMorgan Chase, another top muni underwriter known for its institutional distribution, also beefed up its retail base recently by tapping into the retail network of Charles Schwab Corp. and extending a 2008 agreement with UBS Wealth Management for an additional two years to 2013. Citigroup accesses retail clients through its own network of nearly 20,000 brokers.

Conversely, the broker-dealer Fidelity Investments benefited from the market dislocation of recent years and ramped up its negotiated underwriting of municipal bonds.

The Goldman-Incapital agreement focuses on traditional tax-exempt products rated investment grade. Build America Bonds, with their long maturities and taxable status, have been more popular among institutional buyers rather than retail buyers. But, if market dynamics shift and individual investors become more interested in BABs, this new venture could "absolutely" be a critical avenue in that space as well, Scruggs notes.

Goldman has led 18 BAB deals this year totaling $7.3 billion, ranking it the third-largest underwriter for the stimulus bonds.

- Where are the indictments?

- Who is paying the press to supress information that is negative.

- Where are the regulators?

- Didn't AMBAC's CEO vouch to congress that their insurances were all in great shape?

- Where are the rating agencies? and why are they downgrading the markets after the bankruptcy and not before?

When AMBAC was busy getting its bankruptcy filing prepared. Wisconsin's Office of the Commissioner of Insurance, or OCI took over AMBAC contracts and obligations without making much more than a peep...in the name of preventing a MUNI bond collapse and frozen issuance market...by doing this it was hoping to help the incompetent by deceiving the market into complacency once again while bringing no new structural stability to the picture in any way. The hope was, lets just get the AMBAC name stabilised or out of the picture and keep the game on the normally scheduled programming. Yes, the charade...was endorsed by the OCI and this is an example of regulated fraud. The fraud is all still there, its still occurring every day and these guys attempted to make sure that this was the outcome. That was their specific goal...let a totally flawed, deceptive, highly inducement oriented product continue to function with NO impediments.

Ironically, we should all already know that by its nature, a market in which someone tries to get your money by locking it up, providing crappy collateral and fuzzy or deceptive documentation, would require them to make some sort of inducements and incentives. "Ok, lets make the gains tax-free in order to find marks to whom to pawn it." Sounds logical to me.

At the very same time as this ponzi scheme is being implemented, the regulator(s) had NO problem with all the major Dealers scaling up their marketing and hype surrounding these products specifically focused on "Mom" and "Pop". Yes, there is no issue there...just lets get this boat back on the water keep it looking like its floating and get people on it...

OCI and the regulators in general did a GREAT job regulating yet another legalized fraud and theft.

Then and now...the not so Federal Reserve was also not so different

Friday, Sept 25, 1931: With the Dow off 191 points from the initial bounce out of the crash, the Fed was up to the same old tricks getting everything wrong and making everything worse...the market would fall well over 50% into 1932 and then reach a sustainable bottom...However, if you review the fed bag of tricks and manipulations in the 20's and 30's they are tame compared to today. The results were horrific. Bernanke, the eloquent amature and deceptive "Me, no I am not printing money. Its coming from reserves." pathologic, will attempt to make Time's man of the year again in 2011 by stealing from all its readers while telling them he is bearing gifts. The antics of the Fed for the day are shown below:

The Fed. Reserve reported gold continued to be "earmarked" for the account of foreign central banks (in effect exporting it from the US); $64M was earmarked up to 3PM on Thursday, bringing the total in the past week to $185M. Foreign and local bill selling reached an "extraordinarily large" total of about $100M on Thursday; bill dealers "advanced their rates sharply in a spell of nervousness;" open market rates rose 1/4% on all maturities but the Fed Reserve maintained its buying rates for bills, and left its rediscount rate at 1 1/2%; this was seen as "a virtual invitation to banks and dealers" to sell bills to it. It's believed the Fed. would welcome a large increase in bill holdings and discounts, in pursuance of its policy of "making money rates extremely easy and increasing the volume of both Fed. Reserve and general bank credit outstanding." - Friday, Sept 25, 1931:

Saturday, January 22, 2011

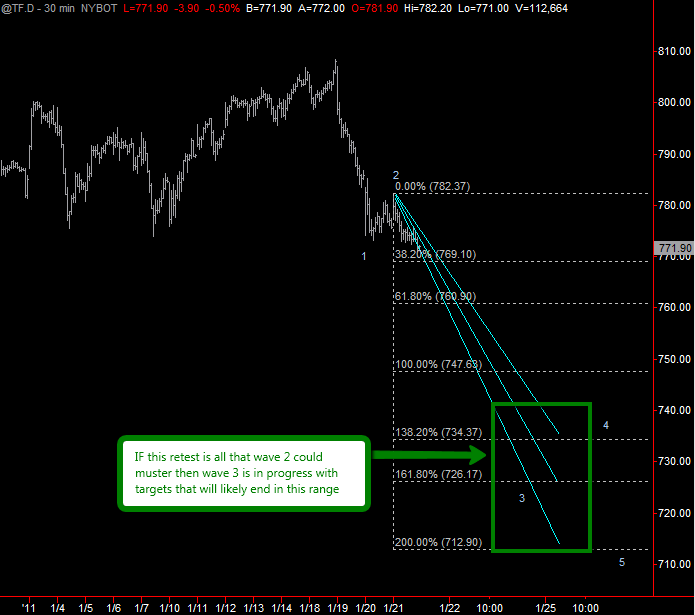

Russell Leads..,

If wave 2 is complete, as it appears to be, then wave 3 has reasonable probabilty points in at these projections. I am currently short TF, ES, NQ, EMD, GOLD, SILVER, Oil among others and added EURO shorts at the end of the week...the systems have not covered with the exception of the Daily TF Swings.

The demise of the EURO continues...

...In case you are wondering why Nigel Farage despises the EU and Herman Van Rompuy, this video exemplifies it.

The major economic and governmental problems we have, center on constant wealth transfer that rewards the incompetent at the expense of the competent and the forced leverage syncronized between banking and government that are the tools that accomplish the job - otherwise known as Fractional Reserve Lending and the Debt Money system.

Whether a person as an individual, or a government as an entity, can legitimately fulfill their obligations is not relevant to people looking to become recipients of their defaulted assets - nor are the attempts to obfuscate the issues and delude the masses. Benanke did not once apologize for cheerleading the Real Estate market all the way down...clearly his agenda was more important than that.

Spain, Greece, Portugal, Italy, Iceland never had a place being considered for a homogenized unit and debt based constitution called the Euro. The presumption that they ever could be forced to maintain compliance and establish economic and constitutional equilibrium was and still is a pipe dream by people attempting to unify finance and governance. This video of Herman Van Rompuy is really a sad commentary on our times. (listen to the quotes at 1 minute and 45 seconds in the video)

After you hear this crap, it rather looks like the hope means "hope for the few" and the "anxiety, uncertainty and lack of confidence" of which they speak are the reasons that they have hope. The crisis that the world is in is not surprise. It has been engineered via regulated and legislated theft and fraud. When I worked at JPMorgan, it was clear that the financial engineering and leverage allowed and encouraged explicitly at the behest of the Fed was being used as a mechanism to scale up and grow our financial system and obfuscate its risks and frailties. This was accomplished via critical accomodative regulatory and legislative efforts and achievments. This leverage was explicitly encouraged, endorsed and allowed.

The result was that a few people have most of the wealth and the remaining people are struggling to cope with the results of their losses. Anxiety, uncertainty and lack of confidence are great tools if you are a banker - especially a pathological central banker who wants to pretend and is determined not to see a housing, debt or derivative bubble even when it's right in front of his eyes.

The major economic and governmental problems we have, center on constant wealth transfer that rewards the incompetent at the expense of the competent and the forced leverage syncronized between banking and government that are the tools that accomplish the job - otherwise known as Fractional Reserve Lending and the Debt Money system.

Whether a person as an individual, or a government as an entity, can legitimately fulfill their obligations is not relevant to people looking to become recipients of their defaulted assets - nor are the attempts to obfuscate the issues and delude the masses. Benanke did not once apologize for cheerleading the Real Estate market all the way down...clearly his agenda was more important than that.

Spain, Greece, Portugal, Italy, Iceland never had a place being considered for a homogenized unit and debt based constitution called the Euro. The presumption that they ever could be forced to maintain compliance and establish economic and constitutional equilibrium was and still is a pipe dream by people attempting to unify finance and governance. This video of Herman Van Rompuy is really a sad commentary on our times. (listen to the quotes at 1 minute and 45 seconds in the video)

"We are in a period of anxiety, uncertainty and lack of confidence. Yet these problems can be overcome by a joint effort in and between our countries. 2009 is the first year of global governance and the climate conference in Copenhagen is another step towards the global management of our planet. Our mission, our presidency is one of hope supported by acts and by deeds." - Herman Van Rompuy

After you hear this crap, it rather looks like the hope means "hope for the few" and the "anxiety, uncertainty and lack of confidence" of which they speak are the reasons that they have hope. The crisis that the world is in is not surprise. It has been engineered via regulated and legislated theft and fraud. When I worked at JPMorgan, it was clear that the financial engineering and leverage allowed and encouraged explicitly at the behest of the Fed was being used as a mechanism to scale up and grow our financial system and obfuscate its risks and frailties. This was accomplished via critical accomodative regulatory and legislative efforts and achievments. This leverage was explicitly encouraged, endorsed and allowed.

The result was that a few people have most of the wealth and the remaining people are struggling to cope with the results of their losses. Anxiety, uncertainty and lack of confidence are great tools if you are a banker - especially a pathological central banker who wants to pretend and is determined not to see a housing, debt or derivative bubble even when it's right in front of his eyes.

Germany - not an island in the rough...

Germany is certainly in better shape than Spain or Greece, however with banks like Deutschebank waiting to blow up and with more off-balance sheet and derivatives risk than a lot of notorious offenders in the US, things are not what they are hyped up to be. Interestingly the DAX has not made an effort to even broach the 8136 high (double top) that it established in 2000 and 2007. This is despite all the trumpeting of salacious and highly laundered numbers in addition to the sundry government interventions and simulations that are supposedly imparting an economic situation in Germany that is "THE BEST EVER"...really? Apparently, that is not believed by everyone...

China and India can not continue to remain bastions and consumers of Germany's and the world's wares when they are suffering their own huge market dislocations, credit bubbles, real-estate bubbles and the widest ever disparity between rich and poor. The seeds are sown all over the modern world for social unrest and tumult. No country can be an island with customers who are as at risk as this.

China and India can not continue to remain bastions and consumers of Germany's and the world's wares when they are suffering their own huge market dislocations, credit bubbles, real-estate bubbles and the widest ever disparity between rich and poor. The seeds are sown all over the modern world for social unrest and tumult. No country can be an island with customers who are as at risk as this.

Friday, January 21, 2011

Fraud continues...no its not better...its worse than ever

As I indicated many times, real estate prices can not stabilize without access to healthy amounts of credit and therefore, will continue decline as long as available credit is inhibited. The essential basis for price increases in real estate of over the last 30 years is the abundance of policy and credit vehicles created by the government and fed. Ironically, the same reasons that education costs have increased as well.

Credit has continued to contract, unless ofcourse you are a primary dealer, fed shareholder or want to buy inflationary assets in the socialized markets. Below is a very interesting graph from Case Schiller and Barry L. Ritholtz's blog of what may be about to happen to the increased leverage that the banks have taken via legalized frauds that have been regulated into being and that allow banks to lower loan loss reserves - counting them as earnings, and also to reflect assets that are worth 5 cents on the dollar at close to par. Keep in mind that IF you believe the banks and take them at their word regrading their assets on their books and the health of their loan portfolio, they are still leveraged much higher than in 2007 in addition to being bigger. But we should not worry, the institutions are much too big to fail now, bonuses are right around the corner and Obama is waiting in the wings with open arms. So, lets just not bother to recognize that banks are nearly universally lying about and overstating asset values and data regarding loan performance/reserve requirements.

So, what happens when a credit fueled rally in real-estate prices is not implemented in the real estate markets? Another 50+% decline in prices, even in Coral Gables Florida and New York, New York and a actualised insolvency of the entire financial and banking system in the US and Europe.

Size and concentration of the banking and financial system...(courtesy: http://jessescrossroadscafe.blogspot.com/)

Credit has continued to contract, unless ofcourse you are a primary dealer, fed shareholder or want to buy inflationary assets in the socialized markets. Below is a very interesting graph from Case Schiller and Barry L. Ritholtz's blog of what may be about to happen to the increased leverage that the banks have taken via legalized frauds that have been regulated into being and that allow banks to lower loan loss reserves - counting them as earnings, and also to reflect assets that are worth 5 cents on the dollar at close to par. Keep in mind that IF you believe the banks and take them at their word regrading their assets on their books and the health of their loan portfolio, they are still leveraged much higher than in 2007 in addition to being bigger. But we should not worry, the institutions are much too big to fail now, bonuses are right around the corner and Obama is waiting in the wings with open arms. So, lets just not bother to recognize that banks are nearly universally lying about and overstating asset values and data regarding loan performance/reserve requirements.

So, what happens when a credit fueled rally in real-estate prices is not implemented in the real estate markets? Another 50+% decline in prices, even in Coral Gables Florida and New York, New York and a actualised insolvency of the entire financial and banking system in the US and Europe.

Size and concentration of the banking and financial system...(courtesy: http://jessescrossroadscafe.blogspot.com/)

Massive reward for failure...bonuses to fly with abandon

As long as the ECB is meeting expect the EURO to be levitated.

I smell some special interest trading desks and banks getting very nice bonuses and a lot of policiticans high-fiving and back slapping. I am rather interested to see how the markets and public treats them...I expect not too well will be the answer.

Thursday, January 20, 2011

Eating Wheat Gluten Causes Symptoms in Some People Who Don't Have Celiac Disease

Irritable bowel syndrome (IBS) is a condition characterized by the frequent occurrence of abdominal pain, diarrhea, constipation, bloating and/or gas. If that sounds like an extremely broad description, that's because it is. The word "syndrome" is medicalese for "we don't know what causes it." IBS seems to be a catch-all for various persistent digestive problems that aren't defined as separate disorders, and it has a very high prevalence: as high as 14 percent of people in the US, although the estimates depend on what diagnostic criteria are used (1). It can be brought on or exacerbated by several different types of stressors, including emotional stress and infection.

Maelán Fontes Villalba at Lund University recently forwarded me an interesting new paper in the American Journal of Gastroenterology (2). Dr. Jessica R. Biesiekierski and colleagues recruited 34 IBS patients who did not have celiac disease, but who felt they had benefited from going gluten-free in their daily lives*. All patients continued on their pre-study gluten-free diet, however, all participants were provided with two slices of gluten-free bread and one gluten-free muffin per day. The investigators added isolated wheat gluten to the bread and muffins of half the study group.

During the six weeks of the intervention, patients receiving the gluten-free food fared considerably better on nearly every symptom of IBS measured. The most striking difference was in tiredness-- the gluten-free group was much less tired on average than the gluten group. Interestingly, they found that a negative reaction to gluten was not necessarily accompanied by the presence of anti-gluten antibodies in the blood, which is a test often used to diagnose gluten sensitivity.

Here's what I take away from this study:

I don't expect everyone to benefit from avoiding gluten. But for those who are really sensitive, it can make a huge difference. Digestive, autoimmune and neurological disorders associate most strongly with gluten sensitivity. Avoiding gluten can be a fruitful thing to try in cases of mysterious chronic illness. We're two-thirds of the way through Gluten-Free January. I've been fastidiously avoiding gluten, as annoying as it's been at times***. Has anyone noticed a change in their health?

* 56% of volunteers carried HLA-DQ2 or DQ8 alleles, which is slightly higher than the general population. Nearly all people with celiac disease carry one of these two alleles. 28% of volunteers were positive for anti-gliadin IgA, which is higher than the general population.

** Some people feel they are reacting to the fructans in wheat, rather than the gluten. If a modest amount of onion causes the same symptoms as eating wheat, then that may be true. If not, then it's probably the gluten.

*** I'm usually about 95% gluten-free anyway. But when I want a real beer, I want one brewed with barley. And when I want Thai food or sushi, I don't worry about a little bit of wheat in the soy sauce. If a friend makes me food with gluten in it, I'll eat it and enjoy it. This month I'm 100% gluten-free though, because I can't in good conscience encourage my blog readership to try it if I'm not doing it myself. At the end of the month, I'm going to do a blinded gluten challenge (with a gluten-free control challenge) to see once and for all if I react to it. Stay tuned for more on that.

Maelán Fontes Villalba at Lund University recently forwarded me an interesting new paper in the American Journal of Gastroenterology (2). Dr. Jessica R. Biesiekierski and colleagues recruited 34 IBS patients who did not have celiac disease, but who felt they had benefited from going gluten-free in their daily lives*. All patients continued on their pre-study gluten-free diet, however, all participants were provided with two slices of gluten-free bread and one gluten-free muffin per day. The investigators added isolated wheat gluten to the bread and muffins of half the study group.

During the six weeks of the intervention, patients receiving the gluten-free food fared considerably better on nearly every symptom of IBS measured. The most striking difference was in tiredness-- the gluten-free group was much less tired on average than the gluten group. Interestingly, they found that a negative reaction to gluten was not necessarily accompanied by the presence of anti-gluten antibodies in the blood, which is a test often used to diagnose gluten sensitivity.

Here's what I take away from this study:

- Wheat gluten can cause symptoms in susceptible people who do not have celiac disease.

- A lack of circulating antibodies against gluten does not necessarily indicate a lack of gluten sensitivity.

- People with mysterious digestive problems may want to try avoiding gluten for a while to see if it improves their symptoms**.

- People with mysterious fatigue may want to try avoiding gluten.

I don't expect everyone to benefit from avoiding gluten. But for those who are really sensitive, it can make a huge difference. Digestive, autoimmune and neurological disorders associate most strongly with gluten sensitivity. Avoiding gluten can be a fruitful thing to try in cases of mysterious chronic illness. We're two-thirds of the way through Gluten-Free January. I've been fastidiously avoiding gluten, as annoying as it's been at times***. Has anyone noticed a change in their health?

* 56% of volunteers carried HLA-DQ2 or DQ8 alleles, which is slightly higher than the general population. Nearly all people with celiac disease carry one of these two alleles. 28% of volunteers were positive for anti-gliadin IgA, which is higher than the general population.

** Some people feel they are reacting to the fructans in wheat, rather than the gluten. If a modest amount of onion causes the same symptoms as eating wheat, then that may be true. If not, then it's probably the gluten.

*** I'm usually about 95% gluten-free anyway. But when I want a real beer, I want one brewed with barley. And when I want Thai food or sushi, I don't worry about a little bit of wheat in the soy sauce. If a friend makes me food with gluten in it, I'll eat it and enjoy it. This month I'm 100% gluten-free though, because I can't in good conscience encourage my blog readership to try it if I'm not doing it myself. At the end of the month, I'm going to do a blinded gluten challenge (with a gluten-free control challenge) to see once and for all if I react to it. Stay tuned for more on that.

{kind=link}

{kind=link}

RVS TF Daily System Short with Level 0 Reticulation (Updated)

The reticulaton engine built the trade that I presented a few days ago and that trade has now progressed to as below.

Wednesday, January 19, 2011

Sorting Through Family Photographs

My garage flooded a few months ago and ruined everything that was on the ground. I know that cardboard boxes are the worst way to store things so I made a point to start opening the ones that were on a shelf to go through each box and sort through everything to either discard, keep or save to send to a family member. This is not an easy task! I spent the entire day going through photographs, cards, letters and old papers. I think I made it through 3 boxes.

One box was filled with every letter my father wrote to my grandparents ("Mama Lois" and "Big John") while he was in college at Oklahoma University. I read a few but knew that I had to put them aside in order to tackle the project at hand. The ones I read were pretty funny. My father asked them to send the local newspaper so he could keep up to date on the local sports in the area (Mama Lois and Big John lived in Spanish Fort, AL at the time) but mostly he talked about working hard in his classes while spending most of his time studying. Riiiiggght......

It was interesting to remember what it was before the technology we have today. Back then, people would sit down to write a letter and wait a week or more to get a response. In today's world, if you don't get a response from a text you sent twenty minutes ago you start wondering what's wrong. He wrote to them a few times a week with about two pages long talking about sports, studying and girls. What else is there to talk about with your parents when you are in college? I look forward to sitting down and reading them all.

It was interesting to remember what it was before the technology we have today. Back then, people would sit down to write a letter and wait a week or more to get a response. In today's world, if you don't get a response from a text you sent twenty minutes ago you start wondering what's wrong. He wrote to them a few times a week with about two pages long talking about sports, studying and girls. What else is there to talk about with your parents when you are in college? I look forward to sitting down and reading them all.

Here are some of my favorite photographs that I found so far. It's funny how technology can turn your photographs the way they once were. Now and days, the only clue to when a photograph was taken is with the clothing and hair styles.

Here are some of my favorite photographs that I found so far. It's funny how technology can turn your photographs the way they once were. Now and days, the only clue to when a photograph was taken is with the clothing and hair styles.I am very fortunate to have these reminders of the people who are no longer physically with me. I look forward to finding more "treasures" and I would encourage you to do the same.

The photograph on the top is my father sunbathing in 1967, "Mama Lois" (Father's mother) camping in 1963, my mother and father in 1968, "Big John" (Father's father) and me in 1972, Both Grandfathers ("Poompa" and Big John") in San Diego in 1965, "Big John" with his car and "Mama Lois"(Dad's Mother) and my dad in 1962 - his letter writing years in college.

Subscribe to:

Posts (Atom)